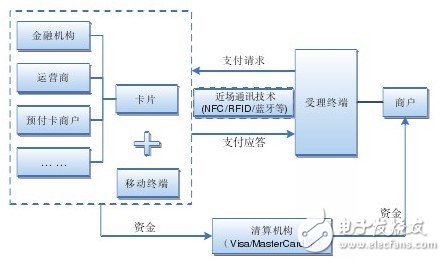

NFC mobile payment mode analysis

As a close-range communication, NFC technology has played a major role in the field of mobile payment. As an NFC near-field payment mode application, NFC mobile payment must be used with bank cards, NFC smart terminals, NFC technology and acceptance terminals. At present, bank cards and NFC smart terminals have been combined to make mobile payment more convenient and faster. The specific mode of NFC payment is as shown in the following figure:

First, the fund account

Since the fund account may belong to a bank or operator, it may also belong to a third-party payment institution. Therefore, the binding of the fund account requires certain technical support, and the security and convenience of the account need to be guaranteed:

1. Fund account security requirements

As a security carrier for financial payment accounts and payment applications, it is required to comply with international CC EAL4+ certification and EMVCO certification. Such chips should have the following security features: encrypted storage space, anti-SPA/DPA attacks, anti-SEMA/DEMA attacks, anti-timing attacks, active shielding, bus encryption, high and low voltage sensors, high and low frequency sensors, illumination sensors, True random number generator, hardware 3DES/RSA/ECC coprocessor, etc.

2. Encapsulation and representation of the fund account carrier

Smart card chips can be packaged in a variety of media. However, in combination with mobile payment, the way the security chip exists mainly depends on the support capabilities of the mobile terminal. The current mainstream forms are:

(1) The whole terminal is directly solidified in the mobile phone chip or stored in a separate card slot.

(2) The smart SD card is stored in the SD card slot of the mobile terminal.

(3) SIM card mode, the function of multiplexing SIM card.

(4) Terminal accessories, such as combining with mobile terminals through an audio port or a USB port.

Regardless of the form of existence, mature and reliable hardware packaging technology should be adopted, so that the direct access of the security chip cannot be dismantled, and the communication of the security chip can not be detected by the logic analysis instrument to ensure the security of the payment account.

3. Fund account management

One of the biggest features of smart card-based mobile payment is that it can support "multiple applications." That is, a smart card can load and run multiple payment-related applications to meet the needs of users in various aspects, and is really convenient for users. The main services include:

(1) Responsible for application management and application lifecycle management, such as remote application download, personalization and update operations.

(2) Responsible for smart card management and smart card lifecycle management, such as remote lock card and pin card.

(3) Legitimacy and security of the application. It can be foreseen that China's future mobile payment ecological environment must be an environment that is market-oriented, diversified, individualized, constantly innovating, and constantly evolving and changing.

Second, the mobile terminal

In theory, in the NFC credit card mobile payment transaction, the mobile terminal is also a carrier, as long as it has NFC/Bluetooth/RFID and other near field communication functions, it can be traded, and has nothing to do with the operating system of the terminal. However, from the perspective of user convenience, the mobile terminal preferably assists the user in implementing common functions such as balance inquiry, historical transaction inquiry, and storage. In terms of mobile terminals that support offline support, technology evolution will be twofold:

1. Near-field communication technology makes the support for Near Field CommunicaTIon (NFC) more perfect.

2, card management technology, safe reading and writing of cards, and gradually enrich the control of the terminal on the card, providing a human-computer interaction interface with rich content and convenient operation.

Third, near field communication interaction

The choice of NFC near field payment is mainly due to the convenience and security of near field communication technology. Although the smart card can interact with the outside by means of a wireless transmission protocol (such as Bluetooth, RFID, etc.) of 2.4G technology by means of a mobile terminal, the NFC technology based on 13.56 MHz is characterized by fast recognition and transaction conforming to a safe distance. Has become the mainstream choice for offline transactions.

At present, the domestic mobile payment standard is based on the 13.56MHz international standard NFC non-contact near field communication technology. Based on this working frequency, it has mature and complete international and domestic technical standards, and has been widely used in the field of electronic payment.

Fourth, the acceptance terminal

Acceptance terminals are also a very critical part. At present, if there is no terminal, all mobile payments cannot be performed. The key technology of the terminal is the acceptance of performance. At present, most of the applications are built on smart cards, and the terminal needs to be supported during use. Therefore, mobile payment cannot be completed without receiving terminal support.

Cloud technology is currently developing rapidly. It can simulate the terminal principle through cloud technology and combine NFC payment with cloud technology. As such, this business processing logic is realized through the cloud, which can alleviate the pressure on the terminal.

Kitchen Appliance,Small Kitchen Appliance Cooker,Counter Top Electric Cooker,Electric Hotplate Cooker

Shaoxing Haoda Electrical Appliance Co.,Ltd , https://www.hotplates.nl